Determine Client Tax Credit Eligibility with Our SECURE Act Tax Credit Estimator

The SECURE Act 2.0 enhanced the initial SECURE Act by extending valuable tax credits for businesses that adopt a new 401(k) retirement plan and satisfy certain eligibility conditions.

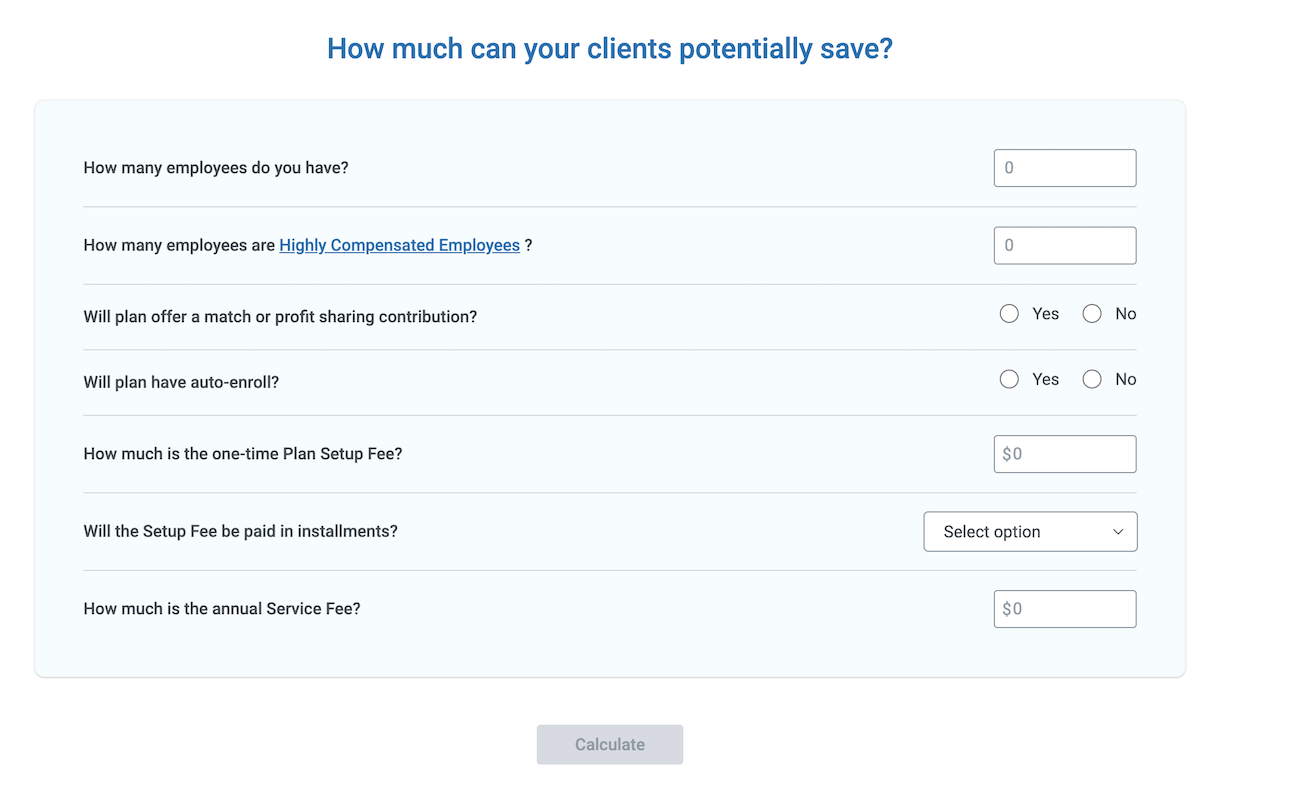

Seasoned financial advisors like you can go above and beyond by estimating your business-owner clients’ eligibility for tax credits right in front of them by using our SECURE Act Tax Credit Estimator.

You can present this information to your business-owner clients to gain their trust and help them realize the benefit of these tax credits. Let’s look at tax credit eligibility requirements and how our SECURE Act Tax Credit Estimator can help determine your clients’ eligibility, boost client advocacy, and increase your business’s stellar reputation.

Key Takeaways:

- Eligible employers can receive several tax credits including new plan startup, employer contribution, and automatic enrollment tax credits.

- Your clients may not be aware of their savings potential, but you can show them the SECURE ACT Tax Credit Estimator.

What are the eligibility requirements to earn tax credits?

Eligible employers can receive up to $5,000 in tax credits for the first three years when they establish a new retirement plan. This is called a retirement plan start-up cost tax and can offset the costs of setting up and administering a new plan. But what makes an employer eligible? The criteria are as follows:

- The employer has had 100 or fewer employees earning at least $5,000 in the previous year.

- The employer has at least one employee who is a non-highly compensated employee, (an employee who earns less than $150,000 per year).

- The employees of the employer did not receive contributions from another employer-sponsored plan in the three years before the new plan startup.

Employers with 1-50 employees are eligible to receive a startup credit of up to 100% of the costs to set up and administer a new retirement plan, while employers with 51-100 employees are eligible for a credit up to 50% of the costs.

Employers may also be eligible for an employer contribution tax credit. Employers with 50 employees or less may receive a tax credit of up to $1,000 per employee when they make matching or profit-sharing contributions. The credit is available on a decreasing basis over a 5-year period.

- For employers with 51 to 100 employees, that tax credit is reduced by 2% for each additional employee after 50.

The final tax credit that eligible employers can receive is for automatic employee enrollment. Employers who add an auto-enrollment feature to their new or established 401(k) plan can earn a tax credit of $500 per year for three years.

How can the SECURE Act Tax Credit Estimator determine eligibility?

Your clients may not be aware of how much they could receive in tax credits. As their advisor, you can sit down with them, ask them a few questions about their business, and enter their information into our SECURE Act Tax Credit Estimator. Eligible clients can potentially receive thousands of dollars in tax credits.

Conclusion

Our SECURE Act Tax Credit Estimator is just what you need to show your clients that they are potentially eligible for numerous tax credits. Opening your clients’ eyes to the valuable tax credits that come along with offering a 401(k) plan will likely position you as someone they can trust. In return for your great service, you could receive both client advocacy and a boosted reputation of excellence.