What Is a 401(k) Plan?

Imagine grabbing lunch with a group of coworkers. Everyone is discussing their 401(k) accounts and their retirement savings goals. You don’t understand the inner workings of a 401(k) plan, and therefore, you’ve chosen not to participate in your company’s plan.

Hoping your colleagues won’t ask for your opinion, you keep quiet as your anxiety grows. Does this scene hit too close to home? We’re here to help you join the conversation by arming you with all the 401(k) information you need.

Key Takeaways:

- A 401(k) plan is a retirement plan benefit provided by your employer.

- 401(k) plan contributions are automatically deducted from your paycheck and transferred to your retirement account.

- Participating in a 401(k) plan can help lower your taxable income.

- Early withdrawals from your 401(k) could result in a 10% penalty; however, there are exceptions to this rule.

- Keeping track of your savings progress is easy with your employee dashboard.

Defining the 401(k) plan:

A 401(k) plan is a retirement savings plan provided by your employer. To participate in the plan, you can either sign up or allow your automatic enrollment. You have control of the dollar amount or percentage that is taken from your paycheck and automatically transferred into it.

With a traditional 401(k) option, your funds are automatically deducted from your pre-tax income. This means every dollar that you contribute to your 401(k) is not taxed until you withdraw it. In other words, a lower income tax payment for you!

Let’s get a little granular, shall we? If you were to invest 10% of each paycheck into your 401(k) account, those funds would automatically be deducted from your paycheck and transferred into your 401(k) account during the payroll process. Your remaining money would be your take-home pay. That 10% deduction in funds equates to less income for you to report during tax season, more importantly, you won’t have to pay taxes on your retirement savings until you make a withdrawal.

If you’ve chosen a Roth 401(k) option, your contributions come from your net, (post-tax), income. In this case, you do have to pay income taxes on every dollar you contribute, but hey, your qualified retirement withdrawals will be tax-free. Not too shabby!

Benefits of 401(k) plan participation:

Aside from potential tax advantages, a 401(k) participant can enjoy other benefits such as:

- Conveniently saving for the future — Automatically contributing to a 401(k) account will allow you to sock away money with ease.

- Employer matching options (if offered)— Employers can match up to 100% of your salary. Don’t leave free money on the table!

- High contribution rates — 401(k) accounts permit a high contribution rate of $23,500 in 2025, allowing you to save more money at a faster pace compared to an IRA.

- High catch-up contributions — After reaching the age of 50, participants can contribute up to an additional $7,500 annually.

- Matured funds over time —When do you hope to retire? The sooner you contribute to your 401(k), the more time your funds will have to mature for your future. Are you aware of the powerful effects of compound returns over time?

- Choosing a Roth or traditional 401(k) account — Do you prefer to lower your tax bill now or in the future? You can decide which type of account would work best for you.

Early withdrawals from your 401(k) account:

While industry experts strongly recommend waiting until retirement to access your funds, there are instances where you’re permitted to withdraw funds early. However, early withdrawals typically result in a 10% fee.

You might be thinking, “but what about in an emergency? I’m going to need money right away.” The government understands that sometimes emergencies happen that require access to your savings immediately.

In that case, there are certain distribution types that won’t require you to pay a 10% early withdrawal fee.

These include:

- Emergency Personal Expense Distribution (EPED)— For your individual or family’s unforeseeable or immediate financial needs.

- Qualified Birth or Adoption Distribution (QBAD)— Intended forchildbirth or adoption expenses of a child (one withdrawal per child in the first year of childbirth or adoption).

- Qualified Disaster Recovery Distribution (QDRD)—A financial loss due to a federally declared disaster, such as losing your home in a wildfire.

- Withdrawals for Domestic Abuse Victims—Must be withdrawn within one year of the domestic abuse incident.

- Distributions taken by a Terminally Ill Individual— Your life expectancy must be 84 months or less.

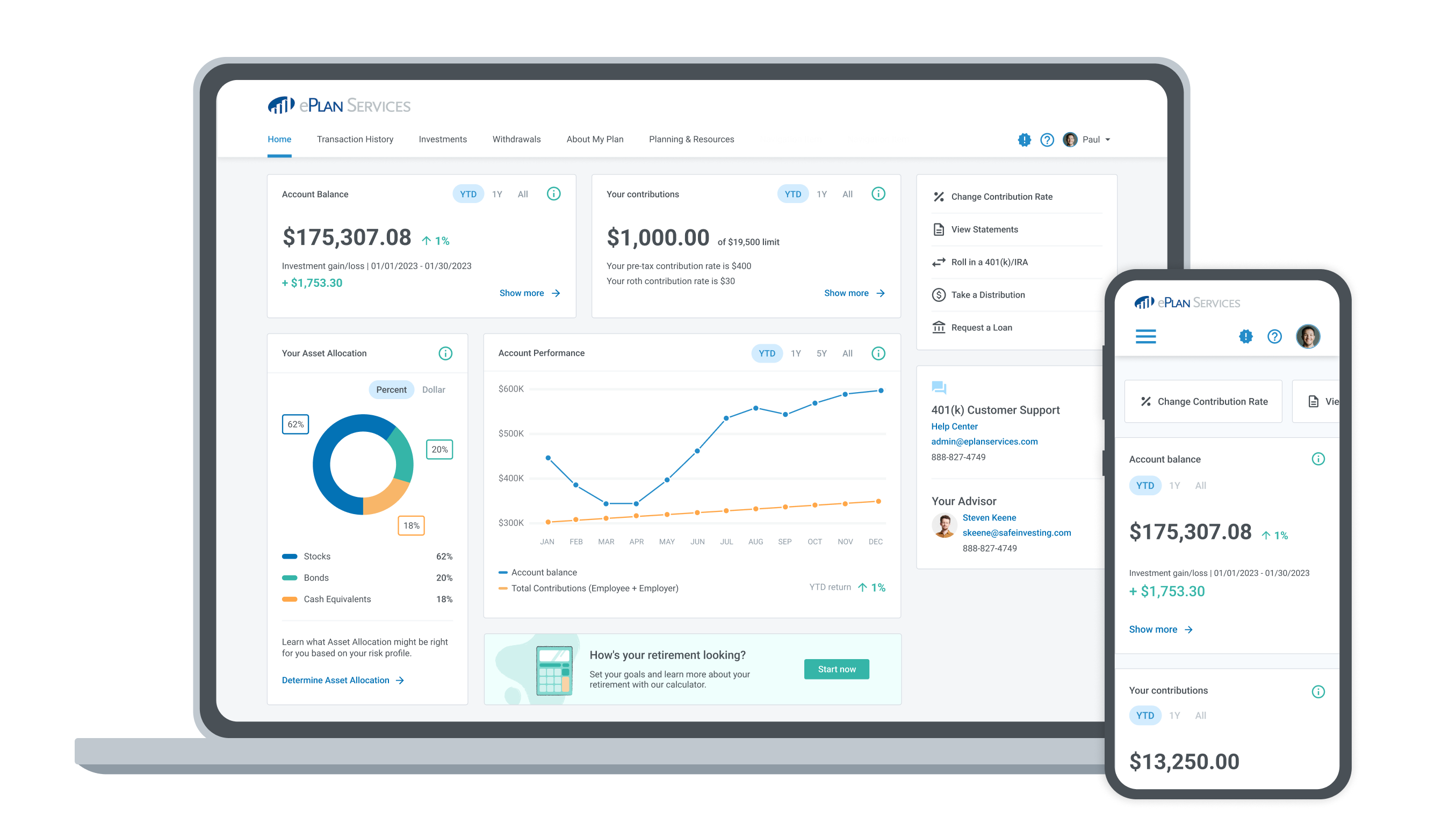

Tracking your 401(k) account performance:

Once your 401(k) account is up and running, take your retirement preparedness even further by keeping an eye on its progress. Sign in to your employee dashboard to view a snapshot of your account balance and even make changes to your contribution rate. You can set your contribution rate as a dollar amount or a percentage.

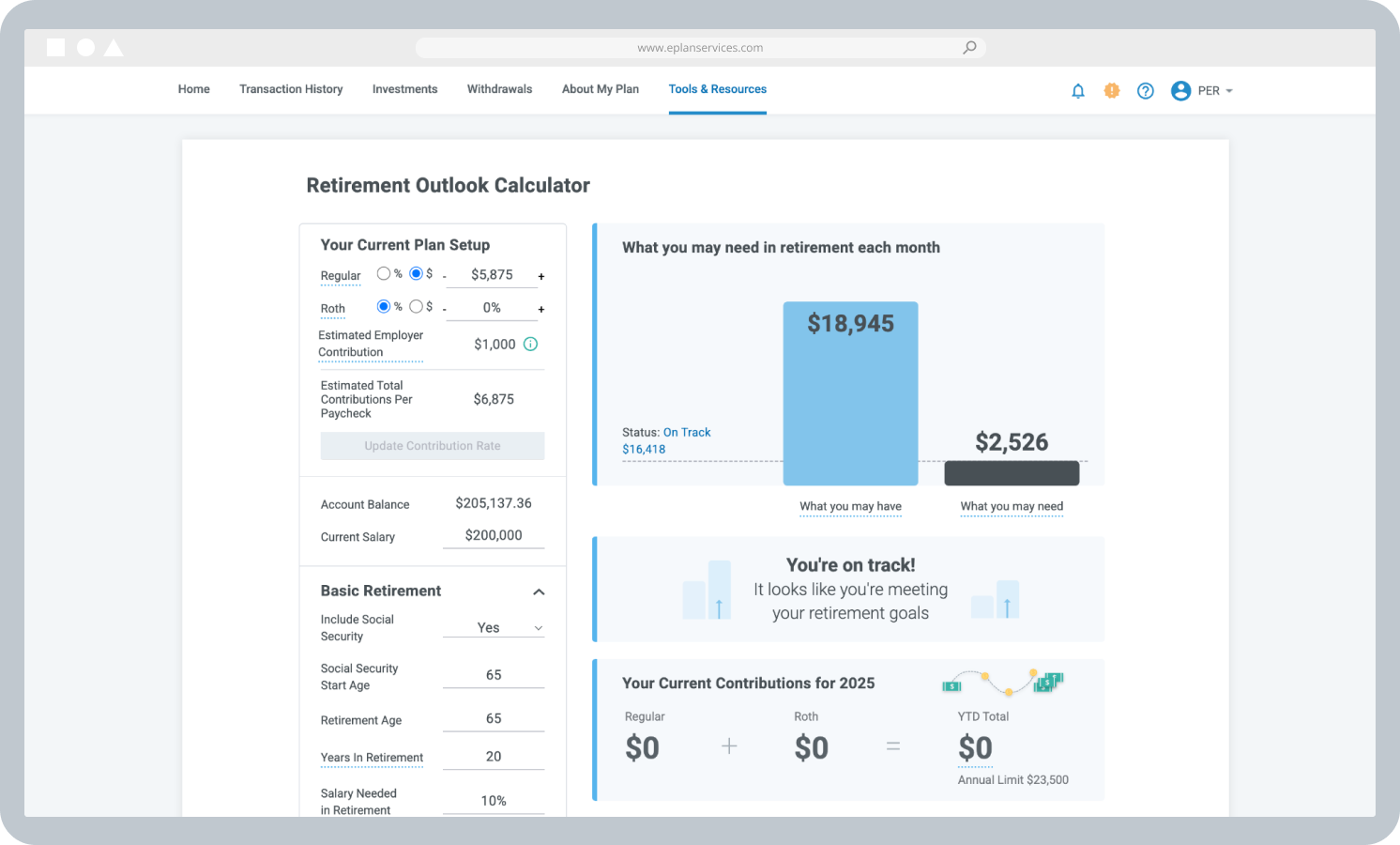

Your dashboard also lets you navigate to your Retirement Outlook Calculator—which shows if you’re on track to reach your retirement savings goal in real time. The calculation is based on factors such as your income, contribution rate, and social security information.

Looking to enhance your retirement outlook? Consider consulting with a financial advisor. They can include your additional investments in the calculation to give you more precise insight into your retirement readiness. We work with a lot of excellent financial advisors and can refer you to an expert: don’t hesitate to reach out!

Conclusion:

Now you can contribute to the 401(k) conversation with confidence! If your employer offers a 401(k) retirement plan, participate now; don’t put it off. Not only are you getting a head start on saving for your golden years, but you’re also lowering your taxable income!